Uncertainty can be part of life, but it would not make things simpler when you are struck by an unpredictable financial emergency. Your car is down. In the vets, the dog winds up. Because of unforeseen conditions, you lose your career. Unforeseen financial emergencies will quickly leave us blind and powerless. If it’s an employment loss, hospital bills, or a home emergency fix, the financial condition suddenly changes can be extremely frustrating.

Even if the situation is difficult, taxes will have to be charged, lights must remain on and food must be on the table. When a financial emergency hits you lately, action should be taken to deal with the adverse economic consequences while reducing it. Moreover, the current prevailing Covid – 19 situations have adverse effects on finances and savings. Following are the steps to deal with a financial crisis:

1. Evaluation of the situation

Once a financial emergency has occurred, take a minute to calm down and assess the condition carefully. It won’t fix something by running around in fear as it brings only tension. A little fear is understandable, you have one million thoughts in your brain, and there is no peace. However, you are likely to make the correct decisions and prevent more difficulties by checking your feelings and carefully assessing the condition at this critical point.

Try to ascertain the root cause of this financial emergency after you have cooled down. You will finally find brainstorming ideas, but first, you need to consider the causes. A sudden reduction of revenue, rising costs that can not be met, and a natural catastrophe can be typical causes. Where any situation will lead to similar crises, the root problem must be dealt with in your course of the attack, or else the wound will simply be re-opened by band-help.

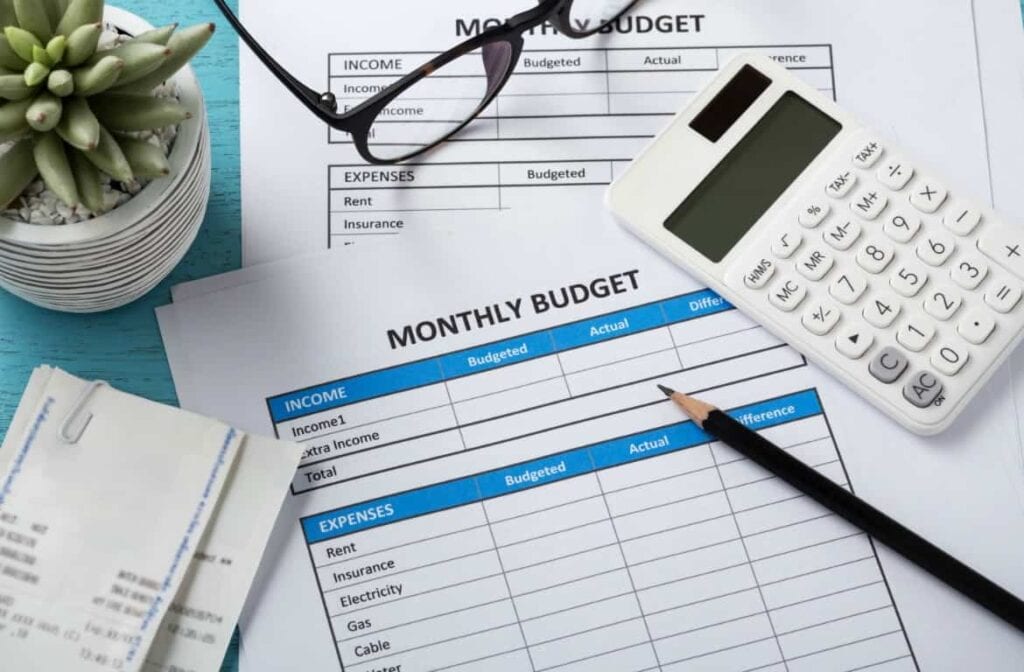

2. Make a budget

A budget is one of the easiest ways to fight financial challenges. A budget is a monthly money expenditure schedule. Making a budget is like changing the lights around a dark space. You don’t have to walk in darkness anymore; you knock your shins, twist around the furnishings and jump on the puppy. You will instead see what’s going on with the lights on to avoid complications before they happen. The same thing happens in a budget; it controls your choices on expenditure so that you spend money on things you care for. In any scenario, you expend your resources so that your financial dilemma will be resolved.

3. Minimize and manage the bills

Maybe this is the time to cut away something you don’t need. You would have less trouble covering your bills if your repetitive monthly costs are as modest as they can be. There is no excuse that late payments or fines are to be paid, but families still do so. You can be extra cautious in this field during a work loss situation. Organized simply will save you a great deal of money in your monthly bills. Set a deadline to check all the accounts twice a month, ensuring that no due dates are missed. Plan paper transfers or e-mail checks to make the deposit more days before the payment is due. This would likely also lead to the bill on schedule if a deviation happens. If you find it difficult to follow all your accounts, begin to compile a list. You will use it after the list is over to ensure you are on top of all your accounts and see if you can consolidate or close any of them.

4. Negotiate with lenders

Contact the lender as soon as possible whether you have problems with credit cards, medical bills, or mortgage payments. Trust it or not, helping you make your payments is in their best interest.

They would like to get more income, even though it means lowering the interest rate or stretching the terms.

One typical error is to hesitate until you reach out to the lenders, and they will not be so keen to deal with you by then. If you know that the budget is tight and you can need support, contact them before payments are made.

5. Find ways to get extra money

Ideally, with an emergency fund, you want enough funds to help cover added expenses, but it isn’t always possible. But, when you tapped on your bank account, where do you turn?

You can still try a credit card or get a loan, but this can only exacerbate the problem if you cannot pay the debt. Although borrowing funds from reliable places like Payday LV can provide rapid access to capital, high premiums and a new monthly payment can also be provided. These additional fees increase the timetable of your financial difficulties, which could make you find yourself in a downward spiral that is almost impossible to retrieve if you borrow too much money. Also, they require a definite income source.

Another choice could be to check with family and friends. Nobody wants to ask for support, but maybe all you need to do with a loved one is a little bit of support. Of note, certain partnerships may also be stressed, so proceed with caution.

6. Increase your liquid savings

This ensures that you can withdraw the funds at any moment without losing money. In addition, unlike withdrawal accounts, when you withdraw the money you will not be faced with early waiver penalties or tax penalties, except for CDs which normally entail that the interest you’ve accrued will be forfeited by you if it closes early.

Don’t spend in stocks or other more risky assets until you have cash on liquid funds for several months. How many months do you need cash? The financial commitments and tolerance of the risk depend on that.

Life is unpredictable, but it must be prepared and vigilant if there is anything you can do to prevent tragedy. You will make a future financial tragedy a fleeting reversal with the right planning.